In this era of epochal transformation and dynamic market shifts, investors have detailed understanding about quantitative valuation models and they consult before making an investment decisions. In the world of human capital, corporate managers have a burden to maximise shareholders value and they need to have similar quantitative detailed understanding of how the market values their company, so they can make equally informed decisions.

Companies while managing their valuations largely focus on improving price-earnings (PE) ratios by driving revenue and margin based on historical heuristics, or summaries of past experiences that aren’t systematically analysed and thus inaccurate. This valuation approach restricts organisation ability to recognise and identify new opportunities and neutralise threats and thus at the same time it handicaps the management teams. This valuation approach has risked capital for many investors in the past and thus lost interest of new investors to intrude capital into their organisation.

The above threats like inability to recognise opportunities and innovate can arise from how their company is valued at its own, differences in how their company is valued compared to competitors across and within the industries, and how their valuation changes over time.

In the era of industrial revolution 4.0, the executives need to change their laggard approach and old thumb rules to efficiently operate their organisation which shouldn’t miss upon new opportunities and fine tune their business models to the market’s changing pitch. If this approach is not transformed, Board of directors might also miss valuable quantitative signals of whether valuation changes are being driven by company or market conditions, and how acclimatise management is to those shifts.

Six Key Valuation Drivers

The six key factors that drive valuation accounts for most of the variability in market valuation and has been an analysis of quarterly data taken out from thousands of companies in hundreds of industries over a period of 20 years. Management teams of the organisation can use these factors to leverage new opportunities and create a universal model that allows them to compare companies across industries, industries and companies within the industry. It also helps leadership team to understand the changes in how the market values any of these companies over time.

Below are the six key drivers of valuation:

- Weighted forecasts of growth in company revenue

- Weighted forecasts of growth in company margin

- Patters of cash returned to shareholders

- Changes in the company’s debt-to-equity ratio

- Economic condition in the particular industry domain

- Volatility of the market in the geographic areas in which the industry’s major companies compete

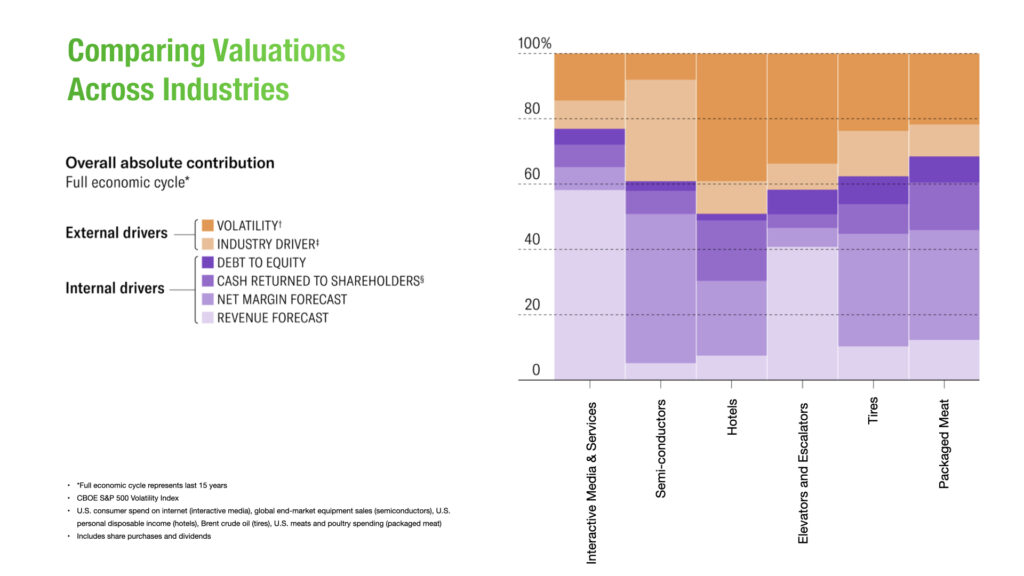

Below graphical representation depicts the comparison of six different industries and shows contribution of each factor to the valuation change.

Out of six factors which are key drivers of valuation four are factors act as an internal driver and two factors act as an external drivers. Four internal drivers that are under the control of a company — revenue forecast, net margin forecast, cash returned to the shareholders and debt-to-equity ration. Remaining two external drivers are not in the control of the company — industry conditions and market volatility in the geographic areas.

Our above analysis confirmed that revenue and margins are generally the most important variables out of the four internal drivers that companies can control, though not in a uniform and balanced manner. The above graphical representation clearly depicts the value of interactive media and services companies is driven by revenue forecast, while that of semiconductor companies is driven mainly by margin. The hotel industry completely relies heavily on margin and cash returned to shareholders.

While in case of elevators and escalators, the revenue forecasts being the prime indicator for valuation, rest in the case of tier and packaged meat the margins remain the prime indicator for valuation.

It’s good for management teams to understand and know what is driving their company, so that they known what to focus on. The above analysis is based on an average across a complete business cycle and offers the truth how companies are analysed.

Key Valuation Drivers Changes as per Dynamic Market

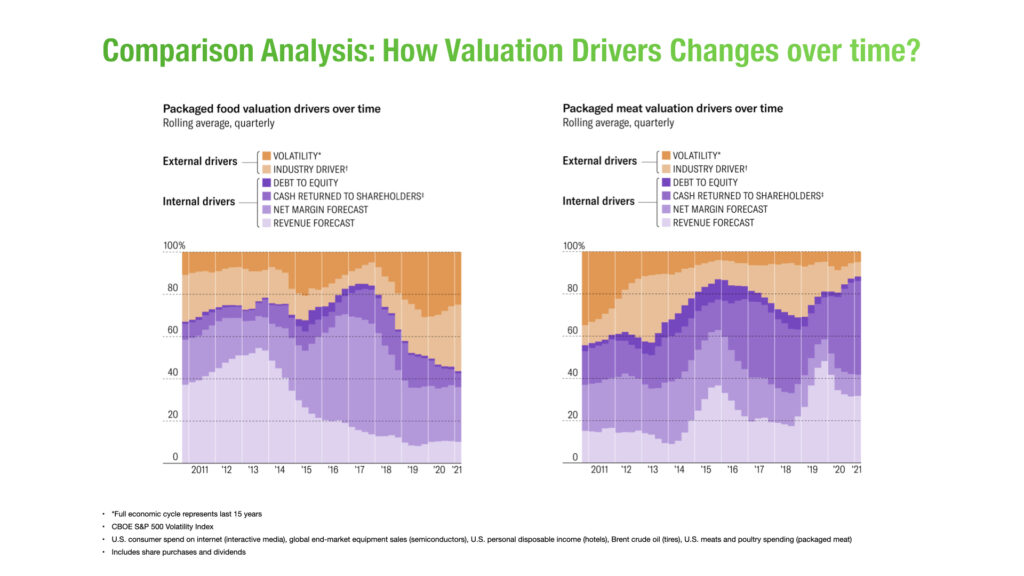

Below is another key graphical representation for the company managers to realise and understand the truth that how these key valuation drivers changes over a period of time. Also, it depicts what are the key factors that drove valuation of packaged food and packaged meat companies from 2011-2020.

Let me put some light on this key example of food industry. The graphical representation clearly indicates that the margin factor being the prime indicator of valuation for packaged food industry over this period while the revenue factor being the prime indicator of valuation for packaged meat industry over this period.

Although firstly the revenue factor was of prime importance for the early investors in 2011 for packaged meat industry but now investors have shifted their interests from revenue to margins which was hardly a matter of prime importance for early investors.

Imagine a packaged meat company hired a new CEO in early 2012, without an analysis of this kind. You find the market is rewarding you for strong margin growth, so that’s where you focus. Over a period of time, the importance of margin growth shrinks and that of revenue growth rises, return suffer. In this world full of massive information, your company’s CEO listen closely to analysts and journalists; and thus he examines PE ratio forecasts. Towards the end of 2017, your organisation CEO focused only on revenue. After a few quarters, things begin to improve. But then the importance of revenue shrinks as cash returned to shareholders begin to dominate, and total returns suffer once more.

How to identify opportunities and threats based on clarity of valuation?

It’s a great message of understanding for companies recruiting CEO from another industry need to know in advance that they’re recruiting a CEO who will design a strategy based not only on past experiences and preexisting beliefs (including about what drives stock value) but also data driven learning about the new industry.

Another learning we discovered for companies recruiting CEO from same industry; CEO might come from one company of the same industry to another company of the same industry would likely to run the company the same way it use to run the previous company of the same industry. In his first company market cares much more about the revenues but for whatever reason now the market demands margins for the second company.

The same clarity of valuation holds true when it comes to merger and acquisitions. Let’s take an example, suppose your company is valued much more on revenue than on margin — but you own a high-margin, low-growth business line that isn’t helping your valuation very much.

Here comes two opportunities for you in place:

- Low-margin, fast-growing business of same industry;

- High-margin, fast-growth business of same industry;

Out of the two opportunities, the second one suites a best-fit opportunity for you is to sell your company in your industry that is predominantly valued based on margin for a great deal more than it is worth to you.

While first opportunity of selling your company to a low-margin, fast-growing business that isn’t worth a great deal to them, you can buy it at a large discount — or find a mutually beneficial swap.