All cash in circulation these days is closely-held by the financial organization and business banks of that currency’s legal jurisdiction, apart from money once within the hands of people.

Banks are trying to survive the languishing sloth created by this innovative technology.

The banking reflects way back after barter and money printing occurred.

If we look at the history of banking and financial systems, they came into authority due to individuals’ trust issues and no centralized power to keep a check on the transactions.

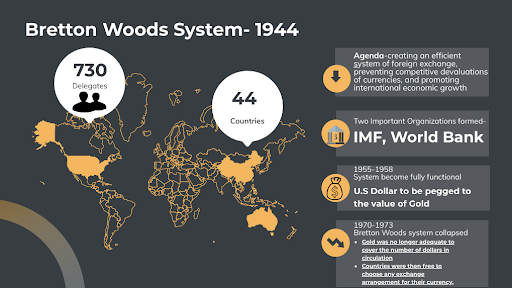

The government enhanced the centralized authority to keep track of such dealings wisely and took hold of cash flow and loans. One major event that led to the transformation and formation of new institutions was the Bretton Woods system.

Learning from the example of the Bretton Woods system:

Earlier in the 20th century, The Bretton Woods system came into view with a mutual agreement with 44 countries.

The incident led to the emergence of regulatory bodies such as IMF and the world bank, and new laws and finances became legal entities.

The Bretton wood agreement created a standard framework by relating it to the valuation of Gold.

A system of fixed exchange rates came into existence where one can compare the value of their currency to USD, which one can peg against the valuation of Gold.

The primary reason for the collapse

- Stabilizing and fixing the exchange rate was not sufficient.

- International transactions and trades were failing due to US reserves.

- The inflationary financial policy was inappropriate for the vital currency country of the system.

- Stabilizing and fixating the rate of exchange wasn’t comfortable.

- Par system created more imbalance and instability.

- It caused more inflation which led to hyperinflation.

Earlier, when the challenges occurred in the Bretton Woods, they led to the collapse. Today’s financial system is facing significant challenges that cannot fit the demands of the time and technology era.

A new ecosystem that replaced the old beliefs and removed many barriers for people by resolving the current financial challenges with acceptance and adaptability of banking systems across the globe.

Financial organizations are typically early adopters of the latest technologies in their business processes.

COVID has already created a scenario toward a shift where old systems might not be able to function the same way.

The coronavirus is shaking the pillars that underpin the temple of the economic process, causing the system to slip off its foundations.

Such a collapse can sometimes be ruinous, and it’s conjointly a chance to plan and construct the international monetary design. So that it’s more resilient to economic shocks – and works towards economic progression.

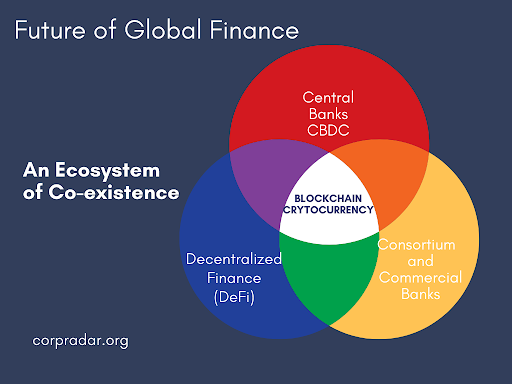

With the present system, Blockchain holds the opportunity to empower economies via a basis of standard technology, which is both Centralized and Decentralized.

Old Financial System | Modern Financial System |

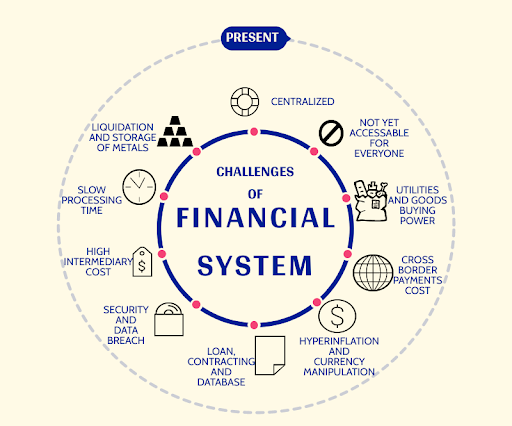

Slow Processing Time: Let’s take a case where business A based in New Delhi, India, wants to procure goods/services from business B, based in the United States of America. The cycle time for the procurement of goods takes around three weeks due to the slow turn-around time of the third parties | Fast Processing Time: Here, business A based in India can directly connect with the supplier, and the intermediaries’ role is minimal. The cycle time comes down from 3 weeks to a couple of days. |

Loan contracting and Database: A person wants to take a personal loan from a Government Bank of his country. He must follow the standard procedure and submit the credit and identification documents required for the verification and risk valuation process. The timeline is a few weeks, and the manual data check is time-consuming for the bank and its customers. Bank Guarantee is required from time to time which requires financial checks for binding the guarantee from one bank to another and finally issued to the person. Intermediaries involvement increases transition time The Database of clients is skeptical about cyber attacks and fishing. | With Digital Ledger Technology and the power of decentralization, it becomes easy for entities to verify a person’s background history and credit score on an immediate basis. Peer to Peer loans and programmed methods reduce the time frame and processing time. P2P loans, credit, infrastructure, insurance-based projects, and services can emerge from such applications of Blockchain. Highly secure and integrated, minimizing the risk of cyberattacks and quickly identifying breaches is possible. Smart contracts can reinvent the process of Bank Guarantee letters . |

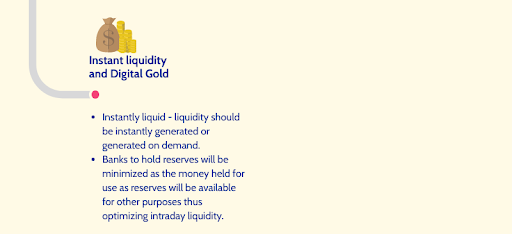

Liquidity and Storage of metals is a costly affair. You can now liquidate your asset into cash or other assets such as bonds or stocks. Banks can hold the reserve with the exchange providers. There may be distress in selling the assets to meet short-term requirements. Gold storage and physical inspection decrease the investment opportunity. For example, A person has Gold in a US bank locker. He is traveling to the UK and needs the direct selling of Gold due to better pricing and urgency to buy other goods. The person cannot access stored metal in the locker. | Instant Liquidity and Digital lockers:

Optimization of intraday liquidity parameters is available with blockchain. The facility of a digital locker integrated with the power of blocks makes it more secure and instant to sell anywhere with application access from your smartphone device. |

The cryptocurrency market cap has already crossed the $3 trillion mark, and emerging cryptocurrency laws by established governments across the planet, formalizing the trade and lowering risks related to crypto investments causing this more isolated acceleration with the emergence of the Central Bank Digital Currency (CBDC)

Several leading central banks worldwide are acting on or considering launching their versions of cryptocurrencies

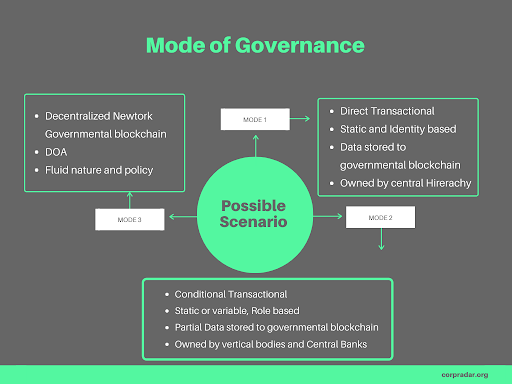

Centralized:

- When the central government is the issuer of the currency known as CBDC()

- Digital illustration of a country’s currency can gain access by an appropriate quantity of financial reserves like gold or foreign currency reserves.

- The central bank maintains its ledger and holds the power of privacy.

- It can be a substitute for current fractional reserve banking and operations.

- Cryptocurrency can be licensed, permission-based, and secure with all policy regulations and frameworks.

- Banks can serve as crypto reserves.

- There’s augmenting demand for private blockchain’s practical application in many business sectors. The suburbanized nature of blockchain produces the modern idea of behavior modification.

Decentralized DeFi:

Innovative developments like Decentralized Finance (#DeFi) and Non-Fungible Tokens (NFTS) It’s peer-to-peer; it doesn’t need powerful intermediaries to evidence or settles transactions.

- While cryptocurrency transactions are units recorded on the DCL, users are a unit solely notable by their virtual addresses, creating them pseudo-anonymous.

- With cryptocurrencies, funds are closely held by those with the keys— this can be an elementary distinction from traditional banking.

- Central banks can empower this with privately-owned financial institutions and involve intergovernmental organizations.

- Business banks might have a task in providing and safeguarding keys—wallets rather than bank accounts. However, their ability to supply deposits to form loans is materially completely different from cryptocurrencies.

- KYC verification method for identification of people

- 70% potential cost saving on financial reporting

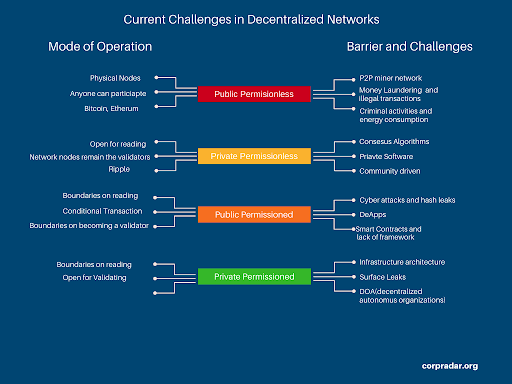

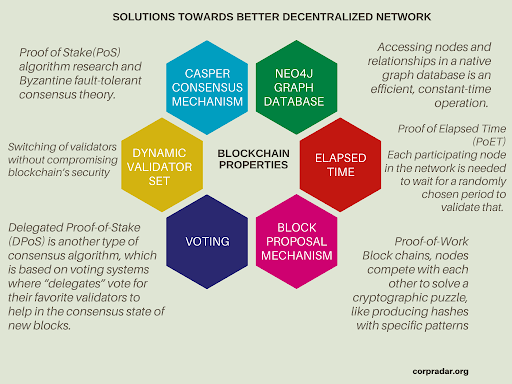

| Significant challenges with the Decentralized system of Blockchain: |

|

|

|

|

|

|

|

Application and Scope of Blockchain:

Accessibility, Efficiency and providing the buying power :

E-commerce platform Integration:

- Over 1M merchants are accepting Crypto as a payment method.

- More than 2.5 B people have access to smartphones and digital devices

- If Brands like Amazon, Walmart will integrate crypto.It can massively change the circulation of cryptocurrencies. It can act as Digital cash.

- 1.7 Trillion of Amazon can lead to cryptovaluations over 500 B and more.

- AVG BTC transaction till 2020 84.3M USD.

- Reduce barriers to capital markets and other financial instruments.

- More control by individuals.

- Steps reduction in execution time can save billions of dollars to both consumer and banks.

Cross Border payment efficiency :

- Cryptocurrency has that potential and valuation where bitcoin can be the next gold. Gold mining is repetitive, and the number is not defined.

- Removes any middlemen and lowers any transaction fees.

- Bitcoin is limited in number and hence creates more valuation.

- 10x more efficient than the current processing fee and time.

- No fiat currency loss takes place during an exchange in the decentralized system.

- In the Defi ecosystem, Digital and peer-to-peer wallet transactions overseas with fees as low as 0.2%.

- It is not yet a real currency, so the inflation problem cannot yet happen because of crypto.

- With appropriate policy and framework, such scenarios will not occur even in the future.

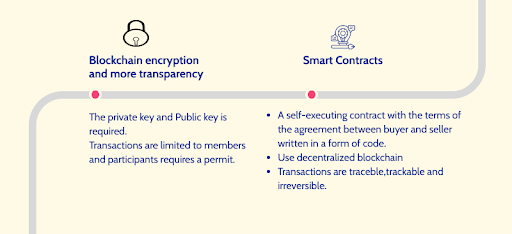

Encryption, Transparency, and Smart Contracts:

Smart Contracts: Cost reconciliation systems and Smart one-one contracts.

- Digital ownership of the data and assets.

- Credit and background history checks based on Ethereum and bitcoin programmable networks.

Domain-specific cryptocurrency:.

- Domain-specific crypto, for example, XYZ crypto for e-commerce, YXD crypto for electricity and utilities.

- Traceable records that can never face manipulation on the ledger.

- Free up working capital.

- No fractional reverse can occur.

- The network effect will only take hold in mature markets by 2025

- Transactions could be limited to participating members that are trackable and irreversible.

- Public and Private distributed ledgers DCL()

Digitized Global Trade and Finance:

- Smart Insurance, Loan provision used in escrow transactions for international trades.

- Escrow payments storing crypto instead of fiat currency

- LC payments restructuring and removal of the manual documentation audit process.Usage of Digital documents with Blockchain integrated systems

- DLT platform for trading.

- The marketplace model can be on Blockchain for trade, shipment, insurance, and financing capabilities.

- Payments to buy utilities from XRP, BTC.

- Digital Gold and Digital Ownership

Future of Global Finance:

Leave a Reply