America has an excess of vacant workplaces.

Presently, a few workplaces face losing WeWork, which has in excess of 600 areas in significant urban communities.

WeWork petitioned for Section 11, Chapter 11, Monday, tossing the eventual fate of the land organization up in the air. WeWork said it would end a portion of its US leases. WeWork’s Chapter 11 will increase the monetary weight on business property managers that have leased enormous lumps of their places of business to the collaborating organization, specialists say.

Office property managers for a really long time hurried to lease space to WeWork, seeing adaptable office spaces as the fate of office life. In any case, these wagers have soured, and some landowners have assumed the obligation to remain above water. About $270 billion in business land credits held by banks will come due in 2023, as per Trepp, a business land information supplier.

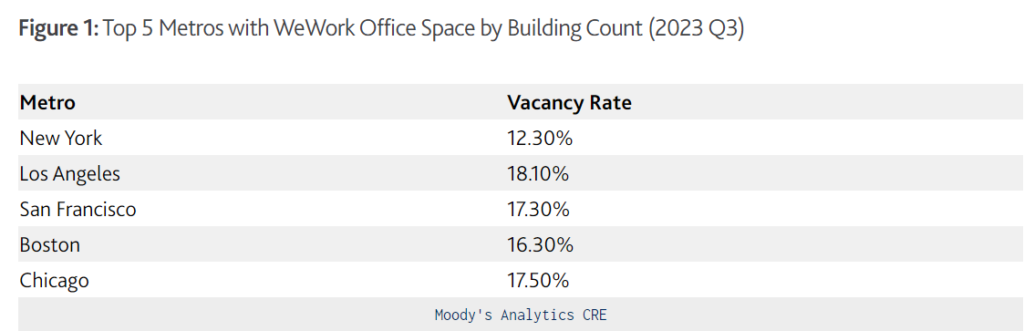

The biggest office markets in the US are likewise the ones in which WeWork has the most properties. While this wouldn’t normally be an issue for a flourishing area where there is a lot of interest and can endure the takeoff of one player, workplaces have really been battling in these metros the most.

Organizations are effectively diminishing their office impressions, driven by lower usage rates as representatives stay away from long drives. While these metros, as framed in Figure 1, have lower opportunity rates no matter how you look at it compared with the public figure, some have encountered a consistent decrease in inhabitance despite everything and still can’t seem to recuperate to pre-2020 inhabitance levels, similar to the case for Los Angeles and San Francisco.

This represents a test for property managers drawing in with capital business sectors with expectations of renegotiating. Execution measurements in certain areas have been frail with misconducts on the ascent (around 5% as of September 2023 for advances 60+ days delinquent).

The qualities at which banks will renegotiate or endorse advances for new office purchases have likely moved downward, putting strain on rates of return, adjusting demeanor, and obtaining choices made by office financial backers. While this conversation has additionally focused on the US office market, WeWork works many properties all over the planet, with many properties rented in every one of a portion of the world’s biggest office markets like London, Tokyo, and Shanghai.

Chapter 11 could meaningfully affect more modest and average-sized banks holding landowners’ obligations, making banks fix advances to home and entrepreneurs, and stirring up financial backer uneasiness about the soundness of the monetary framework.

The breakdown of Silicon Valley Bank and Mark Bank recently sparked fears about banks’ openness to hard-hit business land. Goldman Sachs estimates that 55% of US office credits sit on bank asset reports.

It could likewise hurt civil states that depend on business local charges to offer types of assistance, possibly prompting financial plan cuts. In New York City, for instance, office properties make up 21% of expense income.

“WeWork’s liquidation is a significant shock to the workplace market, particularly on the grounds that the market was in hot water,” said Stijn Van Nieuwerburgh, a land teacher at Columbia Business College. “This is one more colossal issue for the workplace market to battle with.”

No single occupant can represent the moment of truth in the workplace market, he said. Yet, “however much any one occupant can matter, WeWork would be it.”

Urban areas are hit hardest.

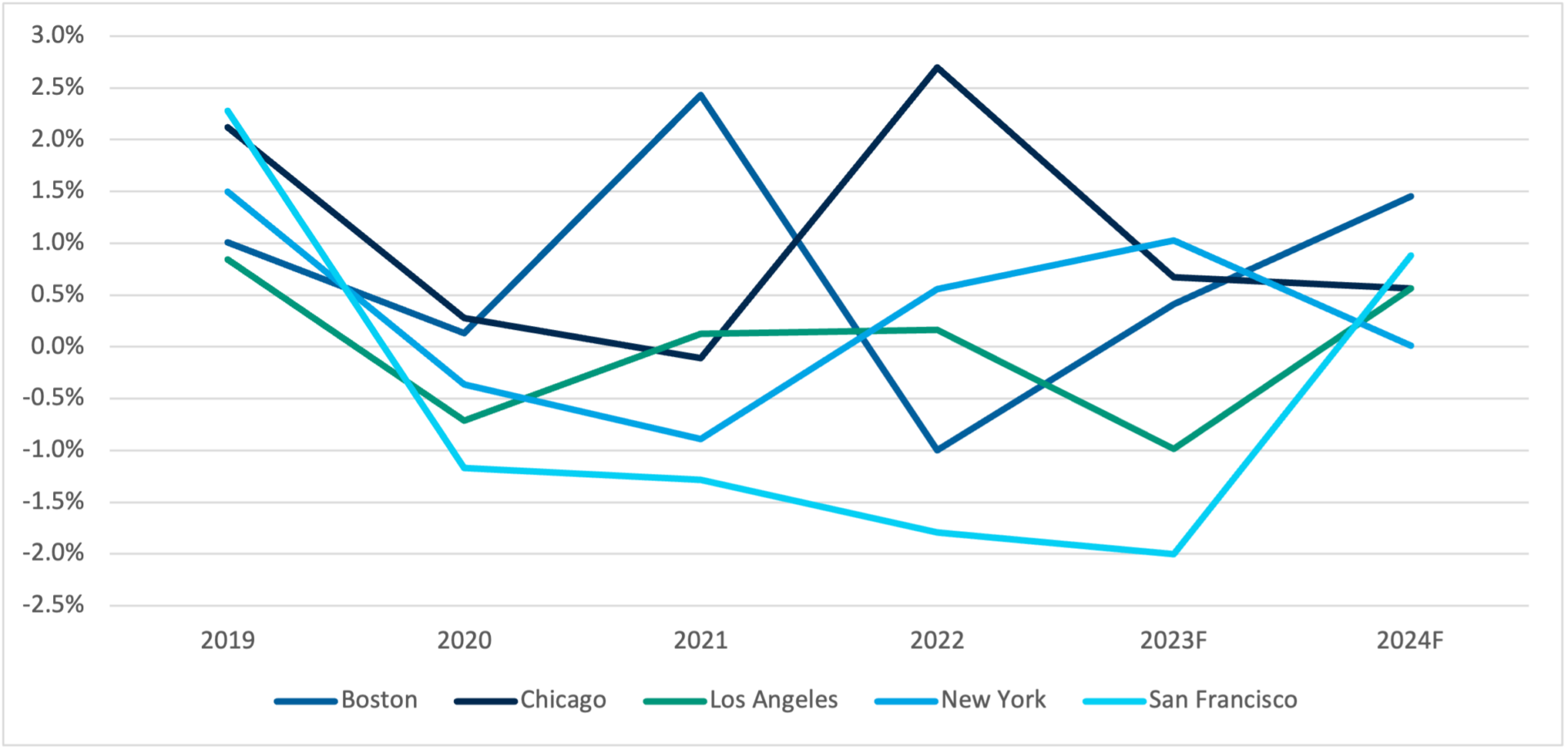

Workplaces in New York City, San Francisco, and Boston will be hit hardest by WeWork’s Chapter 11, specialists say.

Around 42% of WeWork’s inhabitants are in those three urban communities, as per CoStar, a business land information firm. WeWork, as of now, has plans to close 1.9 million square feet in these three business sectors, or around 35% of its total.

In New York City, where WeWork was once the biggest corporate office occupant, WeWork’s dynamic leases are vigorously packed in more established “Class B” structures. These workplaces were at that point considered less engaging for potential occupants than fresher “Class A” resources.

All things considered, 96 years of age, while Class A structures are 48 years of age. Around 65% of WeWork’s leases are in Class B properties, compared with 30% in Class A properties, as per CompStak, a land firm.

WeWork’s bigger openness to Class B structures, specifically, is not great for the New York City office market in light of the fact that many market members are worried about office outdated nature and falling interest in that equivalent class of structures,” Alie Baumann, CompStak’s head of land knowledge, said in an email. In New York City’s Class B structures, for instance, the typical buy size for another arrangement has dropped 36% from 2019 levels.

WeWork’s rents in those structures were likewise higher than the remainder of leases, so property managers can only, with significant effort, recover lost leases from different occupants.

Office market hardships

Business land was hit hard by the pandemic, with fewer individuals getting back to workplaces and burning through cash in midtown hallways. Organizations have diminished their office impressions and reconsidered rents.

The quick expansion in loan fees over the course of the last year has been agonizing for the area since the acquisition of business structures is commonly supported by huge credits.

“It’s the most recent mishap following an extended period of increasing financing costs and elevated degrees of developing obligation,” Baumann said.

Landowners will hope to supplant WeWork with new inhabitants, reasonable at lower rents, yet some will most likely be unable to fill WeWork opportunities.

“Since large numbers of their leases are in Class B structures, where most for the most part concur request is more vulnerable, property managers might confront a difficult task in occupying that space,” she said.

Different proprietors will attempt to switch their structures completely to elective purposes, for example, medical services, advanced education, or lofts. However, changes are troublesome on the grounds that a few structures don’t lend themselves well to, say, new condos or meet administrative prerequisites.

“There are not that many incredible choices,” said Van Nieuwerburgh from Columbia. “I anticipate that Class B and C structures should turn out to be abandoned resources until they go through liquidation and are purchased for pennies on the dollar.”

Source: CNN, Moddy analytics, Fortune